If you've got law firm clients, you already know the work is different. What you might not have sat down and calculated is exactly how different and what that difference is costing you every month against the fee you're charging.

What makes legal bookkeeping different

Solicitors are regulated by the SRA and the rules around client money are strict, specific, and carry real consequences for non-compliance. That compliance burden doesn't sit with the law firm alone. It sits with whoever is keeping their books.

The SRA Accounts Rules require "accurate, contemporaneous, and chronological records" of all dealings with client money. In practice, that means:

- Client money kept entirely separate from office money. A separate client account is mandatory. Every transaction touching client funds has to flow through the right account, correctly coded, every time.

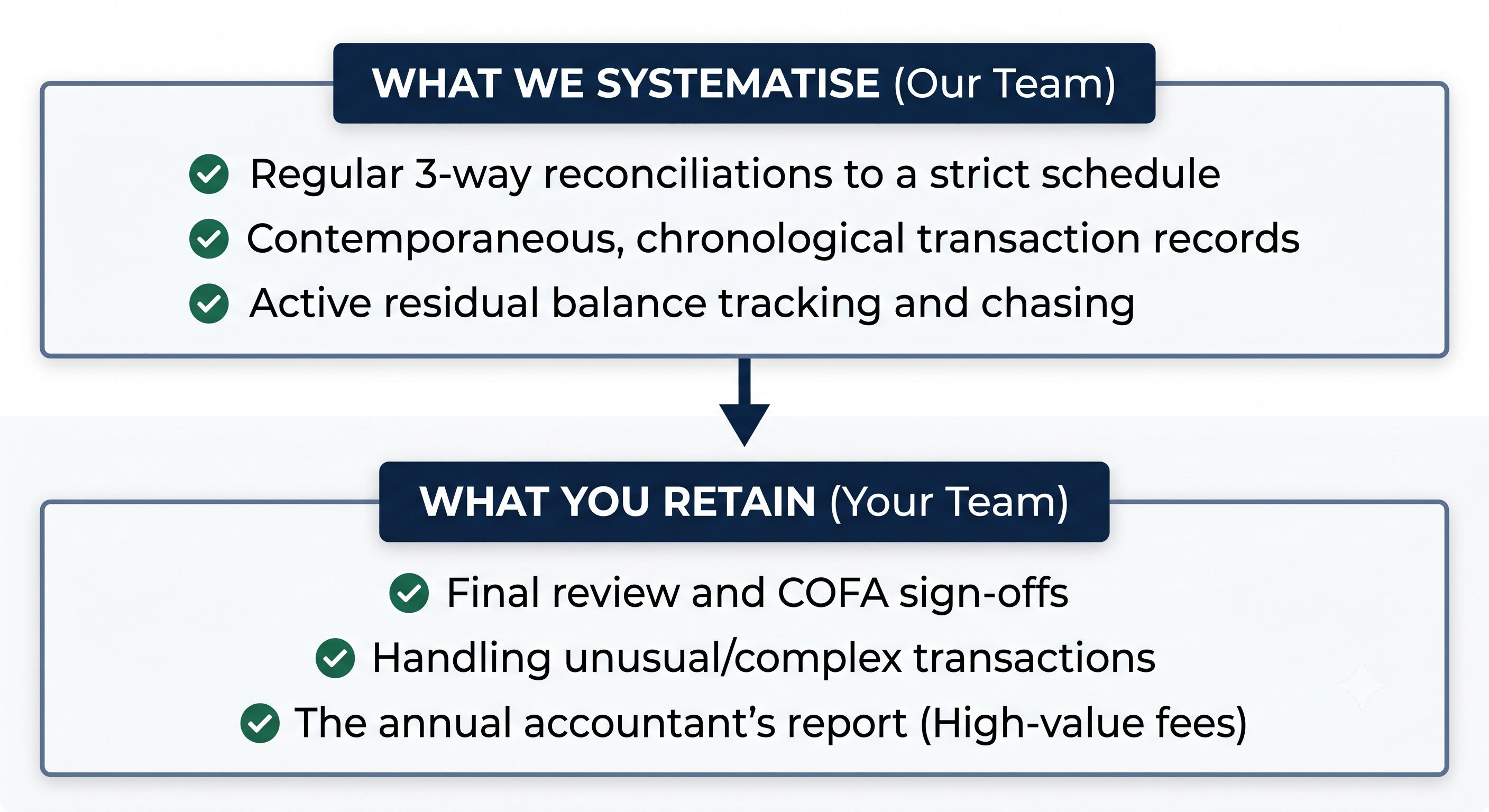

- Three-way reconciliations at least every five weeks. Client ledger, cash book, and bank statement must all agree. This isn't a standard bank rec. It's a significantly more involved process that requires all three to reconcile simultaneously. If they don't, you find out why before you move on.

- Residual balances actively managed. Small amounts left in client accounts at the end of a matter are a recurring compliance breach for many firms. Someone has to track them, chase them, and clear them. That's not a once-a-year job.

- All records stored securely and retained for at least six years. Which means your systems need to handle this correctly from day one.

- A COFA appointed and approved by the SRA. The COFA signs off reconciliations and monitors corrective action. So in theory if the books are behind, that's the COFA's problem. But in practice your law firm client looks to you.

None of this is advisory work. All of it is a recurring, process-heavy administration that lands on whoever is doing the bookkeeping.

The part that should concentrate your mind

If a law firm's bookkeeping falls behind, the reporting accountant who reviews the accounts has a duty to consider whether that should be flagged to the SRA.

This isn't a theoretical risk. Clean, current records are a compliance requirement, not a housekeeping preference. If your firm is the reporting accountant for a law firm client and the books are a mess, you're not just dealing with a difficult client. You're potentially in a position where your own professional obligations come into play.

That changes the nature of the engagement. You're not just doing bookkeeping. You're maintaining a compliance-critical record that your name is attached to.

Where the recovery leaks

The three-way reconciliation alone takes materially more time than a standard bank rec. The client account tracking, the residual balance monitoring, the chronological record requirements: every one of these adds time that a standard business bookkeeping fee doesn't account for.

And because law firm clients tend to have high transaction volumes, with money moving in and out of client account constantly as matters open and close, the workload isn't steady. It spikes. Which means your junior is either on top of it continuously or scrambling to catch up before the five-week reconciliation deadline.

Either way, the time logged doesn't match the fee charged. It rarely does on law firm clients priced as standard bookkeeping work.

What this looks like in practice

We build the SRA bookkeeping workflow once: transaction recording cadence, reconciliation schedule, residual balance tracker, filing structure. Our team runs it under your brand on a rolling basis. Your team reviews, signs off, and handles anything that needs professional judgement.

The result: your law firm clients stop being the ones where your junior is always slightly behind and the five-week deadline is always slightly stressful. And the fee you're charging them starts reflecting the work that's actually going in.